Retire Early On Bitcoin

Are you looking to retire with financial freedom while keeping your wealth secure and growing? This article explores a powerful Bitcoin investment strategy designed to provide a consistent monthly income while maintaining long-term asset appreciation. Learn how to set up an inflation-adjusted benchmark, implement a structured withdrawal plan, and manage volatility with smart strategies like buffer accounts and crypto-backed loans. With discipline and proper execution, Bitcoin can become your ultimate retirement vehicle, ensuring a lifetime of financial security and a lasting legacy. 🚀

11 min read

Bitcoin Retirement Plan

Introduction

In this article, you will learn about an investment strategy that can turn your Bitcoin (BTC) holdings into a consistent monthly income while retaining growth, allowing you to retire comfortably and achieve financial freedom.

Disclaimer: Nothing in this article is financial advice. Do your own research (DYOR) and proceed at your own risk.

Defining Key Goals

Retirement Plan: A strategy that ensures a steady inflow of money for the rest of your life.

Financial Freedom:

1. Your assets are safe, can’t be stolen, destroyed, frozen or controlled by other parties (self-custody).

2. You can spend your wealth anywhere, anytime (borderless)

Requirements for an Effective Retirement Plan

To achieve a sustainable Bitcoin retirement plan, the strategy must:

Provide a consistent income stream.

Allow spending flexibility (anywhere, anytime).

Ensure payouts that keep up with inflation.

Equity also grows by inflation or more

Offer the potential for inheritance, so your financial machine benefits future generations.

Why Use Bitcoin as the Foundation for Retirement?

To retire successfully, we need an asset that appreciates in value persistently over decades. Bitcoin fits this profile due to:

Consistent Outperformance: Bitcoin has beaten inflation by a huge margin and will continue to do so by design (see "Why Invest in BTC"). Fiat has no bottom, so BTC has no top!

Historical Growth: Bitcoin’s compounded annual growth rate (CAGR) over the past 15 years has exceeded 100%, meaning $100 turned into $800 every four years.

Future Growth Potential: While CAGR may now be around 60%, it is expected to stabilize around 20-30% in 10-20 years as Bitcoin's market cap grows into the tens and hundreds of trillions.

Timing Advantage: We are still ahead of widespread adoption, meaning CAGR remains high for a few more years.

Bitcoin Investment Plan for Early Retirement

Determine Your Yearly Income (YI)

Decide how much money you need annually to live comfortably. Be realistic—aiming for "hundreds of millions" isn’t practical, but the plan allows for long-term wealth growth.

Accumulate Bitcoin Until You Reach Your Benchmark

Your goal is to grow your Bitcoin holdings until their total value is 10–12× your yearly income (10× YI). Two popular methods to achieve this are:

Dollar-Cost Averaging (DCA):

Regularly invest a fixed amount, buying more when prices are low and less when high. This smooths your cost basis and reduces the risk of timing the market.Lump-Sum Investing:

If you have substantial capital, investing a large amount upfront can immediately capitalize on Bitcoin’s long-term upward trend.

Combining both strategies can be especially effective: use a lump-sum to gain immediate exposure while DCA mitigates volatility.

Tool to Help You Plan:

Bitcoin Stacking Calculator – Helps estimate how much BTC you need and how long it will take based on your savings rate and BTC price projections.

Implementing the Withdrawal Strategy

Once your Bitcoin holdings reach 10-13x your yearly income need, you can start converting BTC to fiat in a structured way while ensuring long-term growth. However, there are multiple ways of taking profits to enjoy a steady income from your BTC holdings.

Deciding how to withdraw from an investment portfolio is just as important as growing it. A poorly planned strategy can either jeopardize long-term sustainability or limit future growth potential—both of which can have serious consequences.

One common approach is the fixed withdrawal method, where a set amount is withdrawn every month, regardless of market conditions. While this provides a predictable income, it can be disastrous in a downturn. When asset prices drop, more units need to be sold to maintain the same income level, leading to faster depletion of holdings. By the time the market recovers, much of the portfolio may already be liquidated, putting long-term sustainability at risk.

Another strategy is the threshold-based approach, where any excess value above an inflation adjusted benchmark is being sold each time price makes a new high. This method ensures that assets are preserved during downturns, but it also has its flaws. In strong market rallies, it can lead to selling too aggressively, missing out on further upside potential. By locking in gains too soon, it prevents the portfolio from compounding effectively over time, ultimately limiting long-term growth.

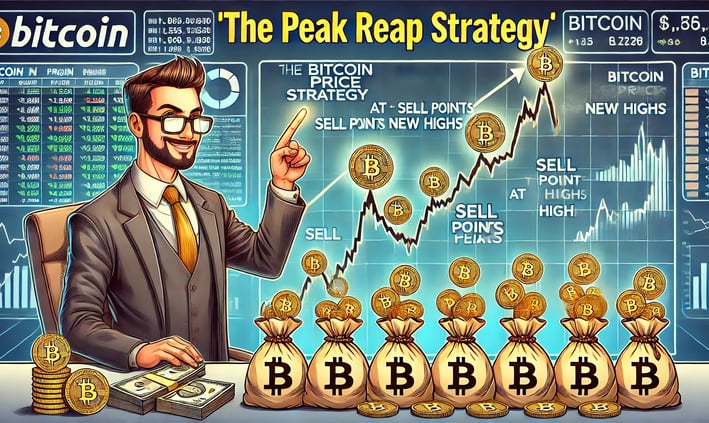

Both methods attempt to balance sustainability and growth, but each falls short in key areas. One risks running out of assets too quickly, while the other misses opportunities for maximizing value. A more advanced approach is needed—one that dynamically adjusts to market conditions while ensuring both security and long-term financial success. The Peak Reap Strategy offers best of both worlds: optimized selling prices, preserved equity growth and long term sustainability.

The Peak Reap Strategy: A Detailed Breakdown

The Peak Reap Strategy is a dynamic, rules-based approach to taking profits from your Bitcoin holdings. It’s designed to capture gains only when prices hit significant new highs, ensuring you sell at premium rates while keeping most of your assets invested for long-term growth.

Tool to Help You Plan:

Use the Peak Reap Retirement Plan Simulator to test the system based on your parameters.

How The Strategy Works:

1. Establish Your Starting Point:

Set an Initial BTC Price: Determine a baseline price for Bitcoin—ideally, the point at which your stack is worth at least 10 times (or more) your yearly income (YI). This gives you a robust starting point.

2. Define Your Sales Triggers and Amounts:

Predetermined Triggers:

When the market price exceeds your initial price by a set percentage - say 3-5% - you trigger a sale.Selling a Portion of Growth:

At each trigger, sell a fixed percentage (for example, 1-2%) of your BTC stack. Note that you are selling a percentage which is less than the growth. It ensures growth both in equity and payouts over time.Optional Initial Buffer Build-Up:

You might choose to wait for a larger increase (say, a 30% jump) before making your first sale. This approach helps you quickly build a substantial buffer account.

3. Repeat the Process:

Each time Bitcoin’s price climbs another 3-5% from your last sale price, you sell another 1-2% of the total USD value.

No Sales on Dips: If the price drops, no sale is triggered, keeping your strategy free from emotional reactions to temporary downturns.

4. Managing Volatility - Buffer Account Mechanics:

Where Do the Proceeds Go?

Every sale’s proceeds are deposited into a dedicated buffer account.

Monthly Payouts

The buffer account is designed to provide steady liquidity by transferring a set amount—say, about 0.83% per month (roughly 10% per year)—to your spending account.

Optimal Buffer Size

The buffer account is designed to provide a steady monthly income, but BTC sales would not always be perfectly timed. To ensure you have enough liquidity for expenses, the account should hold sufficient funds to cover your income needs during bear markets. Given Bitcoin’s four-year halving cycle, it's recommended to build a balance equivalent to approximately three years of income by the end of a bull run…which is why you should begin implementing the strategy when your balance reaches 13 times your annual income – 10X of YI in BTC and 3X of YI in USD. Unless...

Building the Buffer:

If you can wait on receiving regular income, you can start with an empty buffer. The incremental sales will gradually build up this reserve. For instance, if you withhold sales until a 30% price increase, you’ll give your buffer a boost, after which regular sales at each 3-5% price increase will accelerate its growth.

Reinvestment in Bear Markets:

In a strong bull run, your buffer might eventually exceed three years’ worth of income. When that happens, consider using any surplus to buy back Bitcoin during significant dips (for example, spending some on a 30% dip, then increasing purchases with each additional 5% decline).

Why the Peak Reap Strategy Works

Optimized Exit Prices:

By triggering sales only when Bitcoin hits new peaks, you secure high exit prices consistently—avoiding the dilution that comes from selling at mixed price levels.Sustainability:

Because sales occur only at all‑time highs, the amount of BTC sold in each trade is very small. This means you never sell large chunks of your holdings, allowing you to continue benefiting from future growth without depleting your stack too early. Future payouts will keep up with inflation while equity still grows.

New Peaks Keep Coming:

Remember: FIAT has no bottom, so BTC has no top. As long as FIAT money supply is inflated (=forever), BTC (=infinitely scarce) will make new highs. Think about the level of debt worldwide and the new money supply entering the markets every year.

Effective Buffer Management:

The buffer account acts as a safety net. It provides a steady monthly income and absorbs market volatility, so you’re not forced to sell more Bitcoin at unfavorable prices. With a buffer sized to about 3 or more times your annual income, you have a cushion that not only supports you during downturns but also enables strategic buybacks to grow your stack further in bear markets.

Managing Volatility:

Market rewards can come in irregular bursts. The buffer account is designed to bridge the gap between these unpredictable inflows and your regular spending needs. However, during an extended bear market of 3+ years, even a robust buffer built during the bull run might gradually deplete if it's your only income source. In such cases, having alternatives can help sustain your liquidity until the market recovers. So, what can you do after a longer than expected bear market exhausts your buffer?

Leverage Your Holdings: Use your Bitcoin stack as collateral for small, temporary loans (via protocols like AAVE, Compound, MakerDao, or QiDao) to cover monthly expenses. Keep the loans small!! Repay when price peaks again. Use multiple protocols to minimize risk of exploit.

Sell Minimal Chunks: Only as a last resort, consider selling very small amounts—if the price isn’t too low—to meet your needs.

Adjust Spending: Alternatively, rely on other income sources or reduce spending until the next bull cycle kicks in.

Account Management for Security & Convenience

If you self-custody your BTC (instead of using a BTC IRA or another managed service), structure your accounts wisely:

1. BTC VAULT (95-100% of BTC)

Stored in cold storage (hardware wallet).

Never interacts with exchanges or protocols or any addresses other than buffer account.

Maximum security—only withdraw when needed.

2. Buffer Account

Stored in cold storage (hardware wallet).

Interacts with BTC VAULT, Spending Account and exchanges

Holds USD from BTC sales for reinvestment (buybacks) and liquidity (spending).

Acts as middlemen between other accounts

3. Spending Account (Small USD Balance)

Dedicated for debit card spending.

Stored in a wallet connected to debit card. Receive cashback 1-10% of amount spent!

Refill from buffer account in small increments for safety.

4. Exchange Account

Holds BTC (0-5%) to sell according to Reap Peak Strategy

Transfers USD proceeds to Buffer Account (➜ Spending)

Transfers BTC buybacks to Buffer Account (➜ BTC Vault)

The Main Takeaway

The Peak Reap Strategy is all about capturing the best prices by selling only at significant new highs, while keeping most of your Bitcoin invested for future growth. With predetermined triggers (e.g., every 3-5% price increase) and fixed sale percentages (1-2% of your total equity value), it removes emotional decision-making from the equation. The buffer account plays a crucial role by providing steady liquidity for monthly expenses and safeguarding against market volatility. Whether you start with a built-up buffer or allow the strategy to build one over time, this system is designed to be sustainable, maximizing both your selling prices and long-term growth potential.

Custody & Flow Design

This comprehensive flow diagram illustrates our strategic approach to Bitcoin treasury management, highlighting the secure allocation of funds between cold storage and operational accounts. The system maintains 95% of holdings in the secure BTC Vault while utilizing buffer funds for both surplus storage and cash management, ensuring both maximum security and operational flexibility.

Case Study: Alex’s Journey with the Peak Reap Strategy

Meet Alex:

Alex built his Bitcoin stack over the years through dollar-cost averaging (DCA). Today, he holds 10 BTC that he accumulated gradually. With Bitcoin initially priced at $100,000, his portfolio was worth $1,000,000—about 10× his annual income (YI) of $100,000. Now, Alex is ready to implement the Peak Reap Strategy to secure profits at every significant price peak while preserving most of his holdings for long-term growth.

Strategy Parameters:

Sale Trigger: Sell when Bitcoin’s price increases by 3% above its previous all-time high.

Sale Amount: At each trigger, sell 1% of the current BTC stack.

Buffer Account: All sale proceeds go into a buffer account. This account funds monthly payouts (around 0.83% per month, roughly 10% per year) for Alex’s living expenses.

Step-by-Step Execution:

Alex transferred 5% of his holdings from his savings account to the exchange as the price neared his trigger level. For security and privacy reasons, he first routed the funds through his buffer account, ensuring that his savings account never directly interacted with any third-party accounts.

Once his BTC was transferred to the exchange, he placed limit orders to sell in stages at various price levels.

1. First Trigger:

Price Increase: Bitcoin moves from $100,000 to $103,000—a 3% increase.

New Portfolio Value: 10 BTC × $103,000 = $1,030,000.

Action: Alex’s limit order fills and he sells 0,1 BTC (≈$10,300) and deposits it into his buffer account.

Result: Most of his Bitcoin remains invested while a portion of the gains is safely locked away.

2. Second Trigger:

Price Increase: Bitcoin rises another 3% from $103,000 to about $106,090.

New Portfolio Value: 10 BTC × $106,090 ≈ $1,060,900.

Action: Alex sells 1%=0,099 BTC (≈$10,609) and adds the proceeds to his buffer.

3. Ongoing Sales and Buffer Build-Up:

Regular Triggers: Each time Bitcoin’s price climbs by an additional 3% from the last peak, Alex sells another 1% of his remaining stack.

Buffer Role: The cumulative proceeds build the buffer account, which then provides a steady monthly income by transferring about 0.83% of its value to Alex’s spending account.

Optional Initial Boost: If desired, Alex could wait for a larger initial increase (say 30%) before his first sale to build a heftier buffer quickly. However, this delays his monthly payouts.

Projected Buffer Growth with Price Doubling

Imagine Bitcoin’s price doubles from $100,000 to $200,000 over a few years. With a 3% trigger, the simulator estimates around 23 small sales will occur during this increase, each capturing roughly 1% of your portfolio's value. By the time the price reaches $200,000, Alex’s buffer would have grown to approximately $300,000 while his remaining BTC stack is valued at about $1.6 million. This robust buffer not only provides a steady income but also serves as a reserve during market downturns.

For a more detailed, personalized analysis, try our simulator and see how your numbers evolve over time.

Key Takeaways:

Optimized Exit Prices: By selling only when Bitcoin reaches new highs (every 3% increase), Alex locks in profits at premium prices, avoiding the risk of selling during market dips.

Preserved Growth Potential: Since only 1% of the portfolio’s value is sold at each trigger, the majority of Alex’s Bitcoin remains invested, allowing him to capture further price appreciation.

Built-In Safety and Flexibility: The buffer account provides a safety net by accumulating sale proceeds for monthly income and helps cushion against market volatility.

Long-Term Sustainability: Even if the market turns bearish, a well-built buffer (for example, accumulating around $3-400,000) offers multiple options to maintain liquidity and continue the strategy without forced, low-price sales.

Alex’s journey with the Peak Reap Strategy shows how a disciplined, incremental selling plan can help capture high sale prices while preserving long-term growth. By carefully managing the buffer account and having contingency plans for prolonged bear markets, Alex is well-positioned to secure a sustainable retirement income even in the face of Bitcoin’s inherent volatility.

Final Thoughts

Bitcoin provides a viable strategy for retirement if managed correctly. By combining steady withdrawals, long-term growth, and volatility management, you can create a financial machine that sustains you for life while continuing to grow.

However, discipline is crucial to ensuring the success of this strategy. Without strict adherence to the withdrawal plan, reckless spending, or panic selling during market downturns, you risk depleting your Bitcoin holdings prematurely.

To retire successfully with Bitcoin, you must:

Stick to the withdrawal plan – Ensure withdrawals remain at 10% per year, preventing unnecessary depletion of BTC holdings.

Resist emotional decisions – Volatility is a feature of Bitcoin, not a flaw. Avoid panic selling during bear markets and stay focused on the long-term trend.

Maintain proper risk management – Utilize buffer accounts or strategic borrowing to navigate price swings without selling BTC at unfavorable prices.

Keep learning and adapting – The crypto landscape evolves, and staying informed about new financial tools and strategies can enhance your retirement plan.

With the right mindset, patience, and a disciplined approach, Bitcoin can provide you with financial freedom and a sustainable retirement while leaving a lasting legacy for future generations. Bitcoin provides a viable strategy for retirement if managed correctly. By combining steady withdrawals, long-term growth, and volatility management, you can create a financial machine that sustains you for life while continuing to grow. With proper discipline, your BTC holdings will not only secure your retirement but also provide a legacy for your loved ones.